![]()

如何使用#

![]()

[1]:

# !pip install matplotlib pandas pandas_datareader seaborn

# !pip install fracdiff

[2]:

import matplotlib.pyplot as plt

import pandas as pd

import pandas_datareader

import seaborn

seaborn.set_style("white")

[3]:

def fetch_yahoo(ticker):

"""Return pd.Series."""

return pandas_datareader.data.DataReader(

ticker, "yahoo", "2000-01-01", "2020-09-30"

)["Adj Close"]

分数阶微分#

[4]:

import numpy as np

from fracdiff import fdiff

[5]:

a = np.array([1, 2, 4, 7, 0])

[6]:

fdiff(a, n=0.5)

[6]:

array([ 1. , 1.5 , 2.875 , 4.6875 , -4.1640625])

[7]:

np.array_equal(fdiff(a, n=1), np.diff(a, n=1))

[7]:

True

[8]:

a = np.array([[1, 3, 6, 10], [0, 5, 6, 8]])

[9]:

fdiff(a, n=0.5, axis=0)

[9]:

array([[ 1. , 3. , 6. , 10. ],

[-0.5, 3.5, 3. , 3. ]])

[10]:

fdiff(a, n=0.5, axis=-1)

[10]:

array([[1. , 2.5 , 4.375 , 6.5625],

[0. , 5. , 3.5 , 4.375 ]])

通过分数阶微分进行预处理#

[11]:

from fracdiff import Fracdiff

spx = fetch_yahoo("^GSPC") # S&P 500

[12]:

X = spx.values.reshape(-1, 1)

f = Fracdiff(0.5, mode="valid", window=100)

X = f.fit_transform(X)

[13]:

diff = pd.DataFrame(X, index=spx.index[-X.size :], columns=["SPX 0.5th fracdiff"])

[14]:

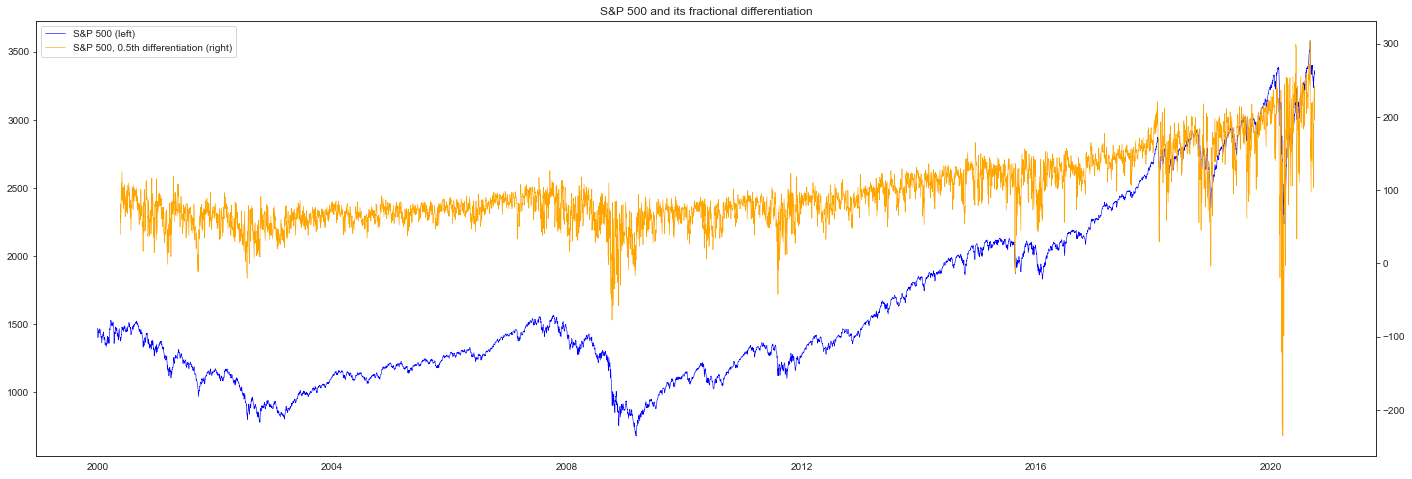

fig, ax_s = plt.subplots(figsize=(24, 8))

ax_d = ax_s.twinx()

plot_s = ax_s.plot(spx, color="blue", linewidth=0.6, label="S&P 500 (left)")

plot_d = ax_d.plot(

diff,

color="orange",

linewidth=0.6,

label="S&P 500, 0.5th differentiation (right)",

)

plots = plot_s + plot_d

ax_s.legend(plots, [p.get_label() for p in plots], loc=0)

plt.title("S&P 500 and its fractional differentiation")

plt.show()

[15]:

from sklearn.linear_model import LinearRegression

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import StandardScaler

np.random.seed(42)

X, y = np.random.randn(100, 4), np.random.randn(100)

pipeline = Pipeline(

[

("scaler", StandardScaler()),

("fracdiff", Fracdiff(0.5)),

("regressor", LinearRegression()),

]

)

pipeline.fit(X, y)

[15]:

Pipeline(steps=[('scaler', StandardScaler()),

('fracdiff',

Fracdiff(d=0.5, window=10, mode=full, window_policy=fixed)),

('regressor', LinearRegression())])

在保留记忆的同时进行微分#

[16]:

from fracdiff import FracdiffStat

[17]:

np.random.seed(42)

X = np.random.randn(100, 3).cumsum(0)

f = FracdiffStat().fit(X)

f.d_

[17]:

array([0.71875 , 0.609375, 0.515625])

[18]:

nky = fetch_yahoo("^N225") # Nikkei 225

fs = FracdiffStat(window=100, mode="valid")

diff = fs.fit_transform(nky.values.reshape(-1, 1))

[19]:

diff = pd.DataFrame(

diff.reshape(-1), index=nky.index[-diff.size :], columns=["Nikkei 225 fracdiff"]

)

[20]:

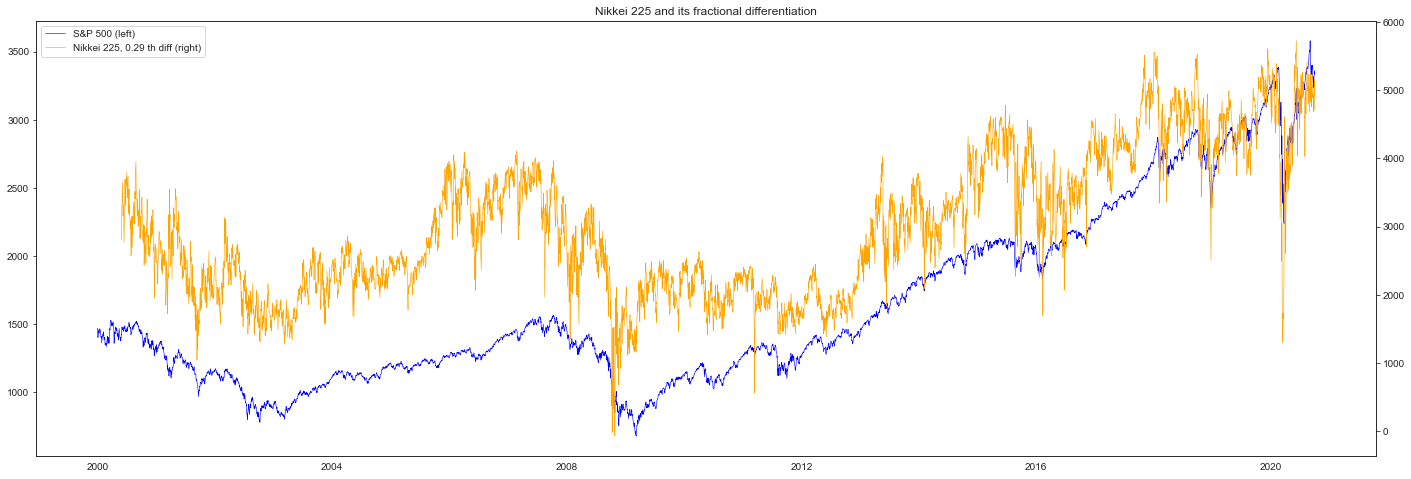

fig, ax_s = plt.subplots(figsize=(24, 8))

ax_d = ax_s.twinx()

plot_s = ax_s.plot(spx, color="blue", linewidth=0.6, label="S&P 500 (left)")

plot_d = ax_d.plot(

diff,

color="orange",

linewidth=0.6,

label=f"Nikkei 225, {fs.d_[0]:.2f} th diff (right)",

)

plots = plot_s + plot_d

ax_s.legend(plots, [p.get_label() for p in plots], loc=0)

plt.title("Nikkei 225 and its fractional differentiation")

plt.show()

[ ]: