![]()

练习#

![]()

[1]:

# !pip install cointanalysis matplotlib numpy pandas pandas_datareader scipy seaborn sklearn statsmodels # noqa: E501

# !pip install fracdiff

[2]:

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import pandas_datareader

import seaborn

from fracdiff import Fracdiff, FracdiffStat, fdiff

from statsmodels.tsa.stattools import adfuller

seaborn.set_style("white")

[3]:

def adf_test(array):

"""Carry out ADF unit-root test and print the result."""

adf, pvalue, _, _, _, _ = adfuller(array)

print(f"* ADF statistics: {adf:.3f}")

print(f"* ADF p-value: {pvalue:.3f}")

5.1#

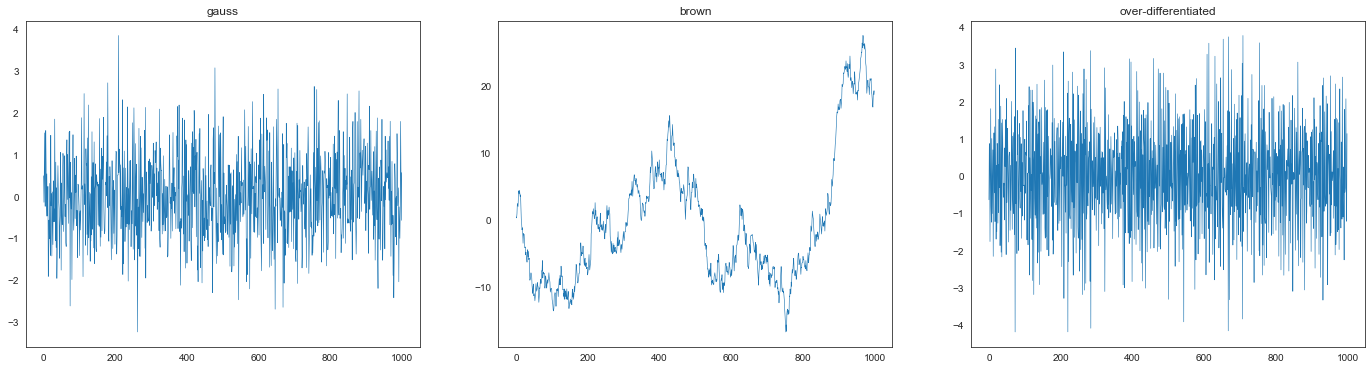

准备高斯分布、其累积和及其微分。

[4]:

np.random.seed(42)

gauss = np.random.randn(1000)

brown = gauss.cumsum()

overd = np.diff(gauss)

[5]:

plt.figure(figsize=(24, 6))

plt.subplot(1, 3, 1)

plt.plot(gauss, lw=0.6)

plt.title("gauss")

plt.subplot(1, 3, 2)

plt.plot(brown, lw=0.6)

plt.title("brown")

plt.subplot(1, 3, 3)

plt.plot(overd, lw=0.6)

plt.title("over-differentiated")

plt.show()

5.1 (a)#

[6]:

adf_test(gauss)

* ADF statistics: -31.811

* ADF p-value: 0.000

5.1 (b)#

累积和的积分阶数为 1。

[7]:

adf_test(brown)

* ADF statistics: -0.966

* ADF p-value: 0.765

5.1 (c)#

过度微分过程的 ADF 统计量和 p 值为

[8]:

adf_test(overd)

* ADF statistics: -11.486

* ADF p-value: 0.000

5.2#

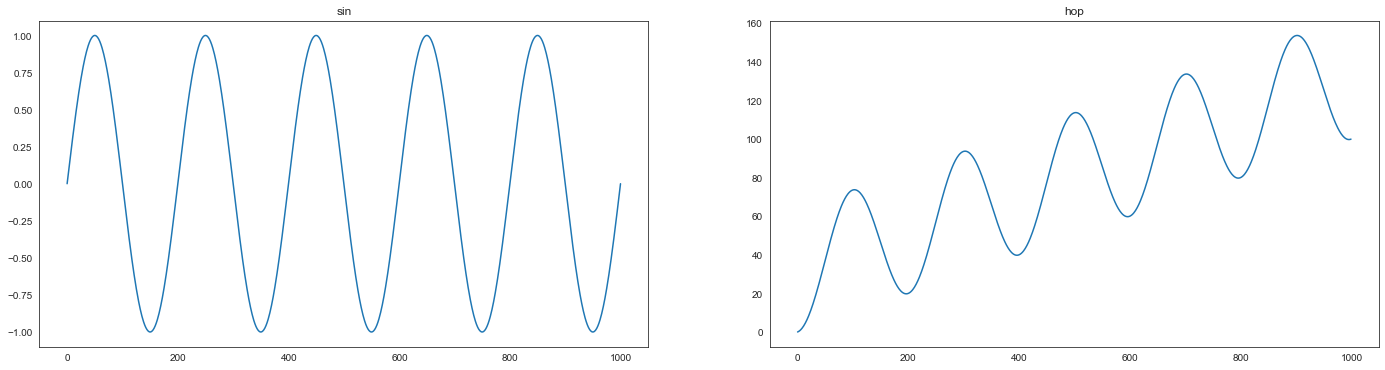

准备

sin函数以及由(sin + shift).cumsum()给出的过程(我们称之为hop)

[9]:

sin = np.sin(np.linspace(0, 10 * np.pi, 1000))

hop = (sin + 0.1).cumsum()

[10]:

plt.figure(figsize=(24, 6))

plt.subplot(1, 2, 1)

plt.title("sin")

plt.plot(sin)

plt.subplot(1, 2, 2)

plt.title("hop")

plt.plot(hop)

plt.show()

5.2 (a)#

[11]:

adf_test(sin)

* ADF statistics: -13323341825676.293

* ADF p-value: 0.000

5.2 (b)#

[12]:

adf_test(hop)

* ADF statistics: -0.284

* ADF p-value: 0.928

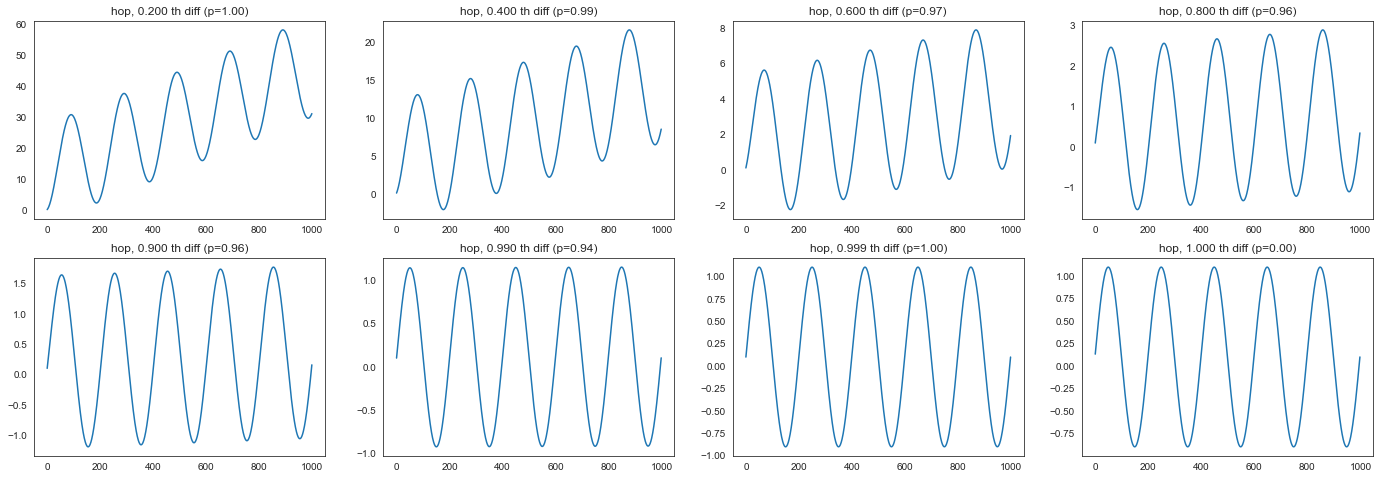

让我们看看

hop在不同阶数下的 fracdiff 的 ADF p 值注意:我们将使用固定窗口方法而不是扩展窗口方法。

[13]:

ds = (

0.200,

0.400,

0.600,

0.800,

0.900,

0.990,

0.999,

1.000,

)

window = 100

X = hop.reshape(-1, 1)

plt.figure(figsize=(24, 8))

for i, d in enumerate(ds):

diff = fdiff(hop, d, window=window)

_, pvalue, _, _, _, _ = adfuller(diff)

plt.subplot(2, 4, i + 1)

plt.title(f"hop, {d:.3f} th diff (p={pvalue:.2f})")

plt.plot(diff)

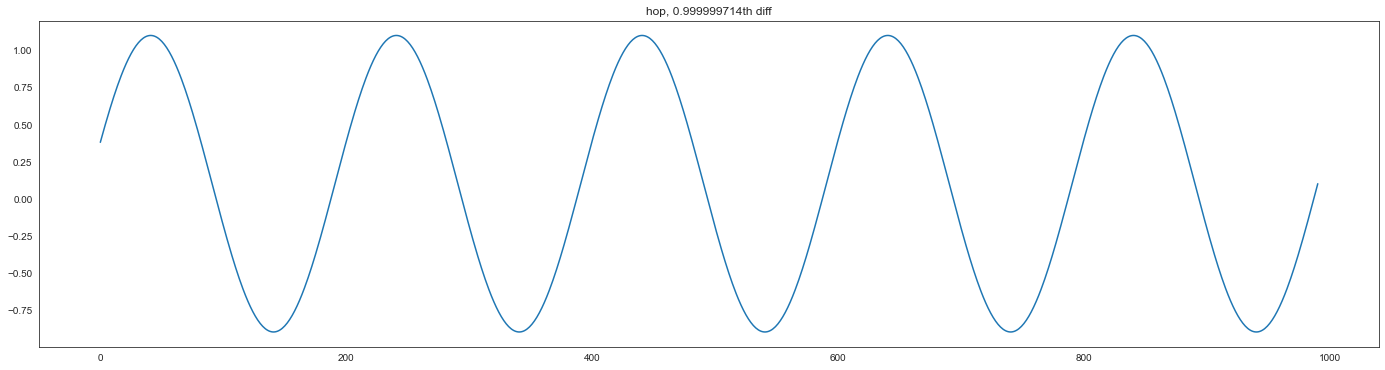

似乎最小阶数非常接近

1.0。让我们使用

FracdiffStat搜索最小值。

[14]:

precision = 10e-8

f = FracdiffStat(window=window, mode="valid", precision=precision, lower=0.9)

diff = f.fit_transform(X)

print(f"* Order: {f.d_[0]:.8f}")

adf_test(diff)

* Order: 0.99999971

* ADF statistics: -280803737.580

* ADF p-value: 0.000

[16]:

# Check

diff = Fracdiff(f.d_[0] - precision, mode="valid").fit_transform(X)

print(f"* Order: {f.d_[0] - precision:.8f}")

adf_test(diff)

* Order: 0.99999961

* ADF statistics: 0.001

* ADF p-value: 0.959

微分后的时间序列看起来像这样

[17]:

plt.figure(figsize=(24, 6))

plt.plot(diff)

plt.title(f"hop, {f.d_[0]:.9f}th diff")

plt.show()

5.3#

5.3 (a)#

[18]:

from sklearn.linear_model import LinearRegression

[19]:

linreg = LinearRegression()

linreg.fit(sin.reshape(-1, 1), hop)

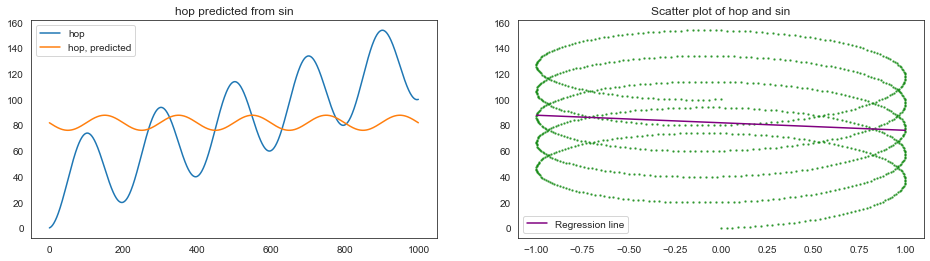

print(f"* R-squared: {linreg.score(sin.reshape(-1, 1), hop):.4f}")

* R-squared: 0.0128

[20]:

plt.figure(figsize=(16, 4))

plt.subplot(1, 2, 1)

plt.title("hop predicted from sin")

plt.plot(hop, label="hop")

plt.plot(linreg.predict(sin.reshape(-1, 1)), label="hop, predicted")

plt.legend()

plt.subplot(1, 2, 2)

plt.title("Scatter plot of hop and sin")

x = np.linspace(-1, 1, 2)

y = linreg.predict(x.reshape(-1, 1))

plt.scatter(sin, hop, s=2, alpha=0.6, color="green")

plt.plot(x, y, color="purple", label="Regression line")

plt.legend()

plt.show()

5.3 (b)#

[21]:

hopd = np.diff(hop)

linreg = LinearRegression()

linreg.fit(sin[1:].reshape(-1, 1), hopd)

print(f"* Coefficient: {linreg.coef_[0]}")

print(f"* Intercept: {linreg.intercept_}")

print(f"* R-squared: {linreg.score(sin[1:].reshape(-1, 1), hopd):.4f}")

* Coefficient: 0.9999999999999994

* Intercept: 0.1

* R-squared: 1.0000

5.3 (c)#

d=1。因为hop的一阶微分是sin加上一个常数。

5.4#

注意:我们将使用时间柱(time-bar)而不是美元柱(dollar-bar)。

[22]:

def fetch_spx(begin="1998-01-01", end="2020-09-30"): # noqa: D103

return pandas_datareader.data.DataReader("^GSPC", "yahoo", begin, end)["Adj Close"]

[23]:

spx = fetch_spx()

[24]:

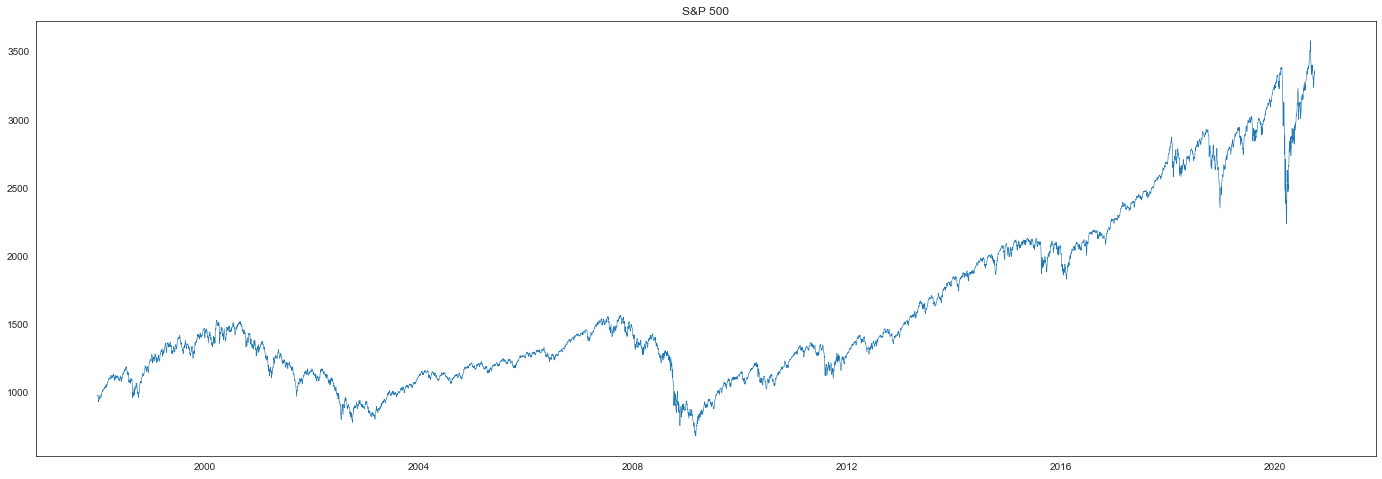

plt.figure(figsize=(24, 8))

plt.plot(spx, linewidth=0.6)

plt.title("S&P 500")

plt.show()

[25]:

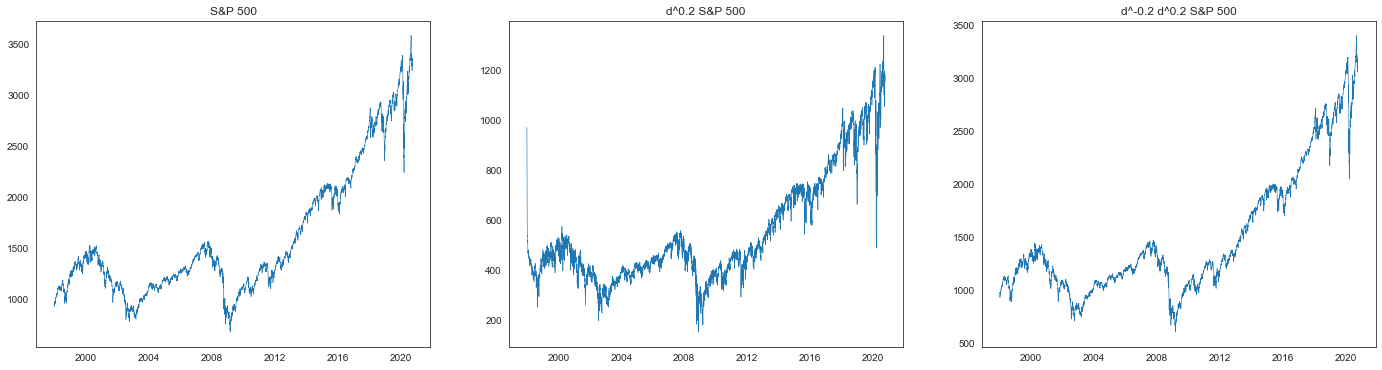

d = 0.2

window = 100

d0 = fdiff(spx.values, d, window=window, mode="full")

d1 = fdiff(d0, -d, window=window, mode="full")

spxd = pd.Series(d0, index=spx.index)

spxi = pd.Series(d1, index=spx.index)

原则上,我们得到的是原始时间序列加上一些常数。

同时,由于有限窗口截断系数序列,会产生小的数值误差。

[26]:

plt.figure(figsize=(24, 6))

plt.subplot(1, 3, 1)

plt.title("S&P 500")

plt.plot(spx, linewidth=0.6)

plt.subplot(1, 3, 2)

plt.title(f"d^{d} S&P 500")

plt.plot(spxd, linewidth=0.6)

plt.subplot(1, 3, 3)

plt.title(f"d^{-d} d^{d} S&P 500")

plt.plot(spxi, linewidth=0.6)

plt.show()

5.5#

5.5 (a)#

[27]:

spxlog = spx.apply(np.log)

spxlogcumsum = spxlog.cumsum()

spxlogcumsum

[27]:

Date

1997-12-31 6.877739

1998-01-02 13.760218

1998-01-05 20.644776

1998-01-06 27.518540

1998-01-07 34.389631

...

2020-09-24 41792.094032

2020-09-25 41800.195243

2020-09-28 41808.312436

2020-09-29 41816.424805

2020-09-30 41824.545394

Name: Adj Close, Length: 5725, dtype: float64

5.5 (b)#

[28]:

from fracdiff.tol import window_from_tol_coef

window = window_from_tol_coef(0.5, 1e-5)

window

[28]:

928

[29]:

X = np.array(spxlogcumsum).reshape(-1, 1)

f = FracdiffStat(window=window, mode="valid", upper=2)

diff = f.fit_transform(X)

print(f"* Order: {f.d_[0]:.2f}")

* Order: 1.73

[30]:

# Check stationarity

adf_test(diff)

* ADF statistics: -2.868

* ADF p-value: 0.049

5.5 (c)#

[31]:

X = spxlog.values.reshape(-1, 1)

f = FracdiffStat(window=window, mode="valid")

spxlogd = pd.Series(f.fit_transform(X).reshape(-1), index=spx.index[-diff.size :])

[32]:

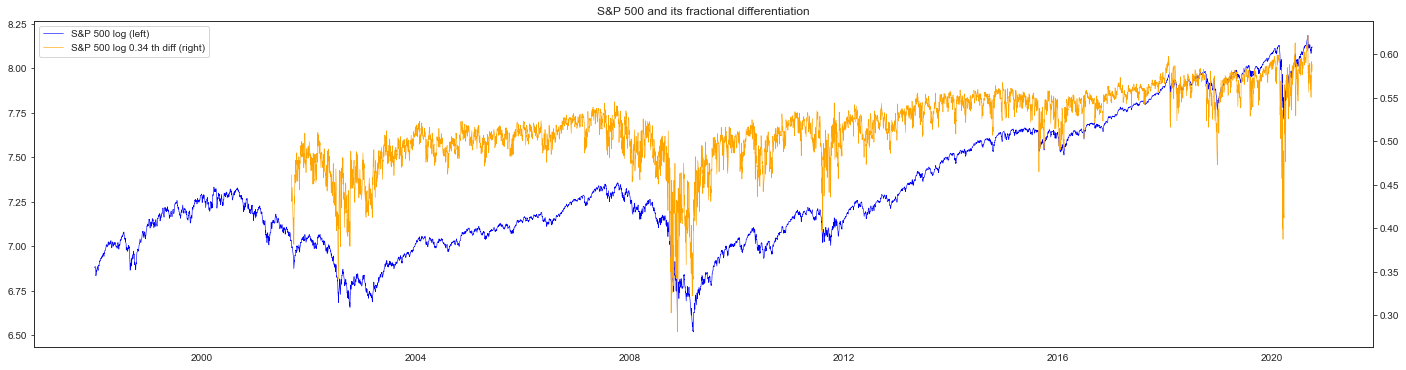

corr = np.corrcoef(spxlog[-spxd.size :], spxd)[0, 1]

print(f"* Correlation: {corr:.2f}")

* Correlation: 0.98

[33]:

fig, ax_s = plt.subplots(figsize=(24, 6))

ax_d = ax_s.twinx()

plot_s = ax_s.plot(

spxlog[-spxd.size :], color="blue", linewidth=0.6, label="S&P 500 log (left)"

)

plot_d = ax_d.plot(

spxlogd,

color="orange",

linewidth=0.6,

label=f"S&P 500 log {f.d_[0]:.2f} th diff (right)",

)

plots = plot_s + plot_d

plt.title("S&P 500 and its fractional differentiation")

ax_s.legend(plots, [p.get_label() for p in plots], loc=0)

plt.show()

5.5 (d)#

[34]:

from cointanalysis import CointAnalysis

讨论

Xd的协整(cointegration)是没有意义的,因为协整定义在非平稳过程之间,而Xd是平稳的。因此,我们将转而讨论 1.3 阶微分后的时间序列(非平稳)与原始时间序列之间的协整。

[35]:

d = 0.30

# Check non-stationarity

diff = fdiff(spxlog, d, window=window, mode="valid")

spxlogd = pd.Series(diff, index=spxlog.index[-diff.size :])

adf_test(diff)

* ADF statistics: -2.445

* ADF p-value: 0.129

[36]:

pair = np.stack((spxlog[-diff.size :], diff), 1)

ca = CointAnalysis().test(pair)

print(f"* AEG statistics: {ca.stat_:.2f}")

print(f"* AEG p-value: {ca.pvalue_:.2e}")

* AEG statistics: -4.26

* AEG p-value: 2.96e-03

它们是协整的。

大致原因:对于

d=0,两个序列完全相同,因此 trivially 协整。对于接近使 fracdiff 平稳的最小值的d,可以通过将原始序列乘以一个无穷小的系数加到 fracdiff 来得到一个几乎平稳的序列。假设插值,可以预期任何介于两者之间的d都会协整。

[37]:

ca.fit(pair)

ys = (-spxlog * ca.coef_[0])[-spxlogd.size :]

yd = spxlogd * ca.coef_[1] - ca.mean_

[38]:

plt.figure(figsize=(16, 4))

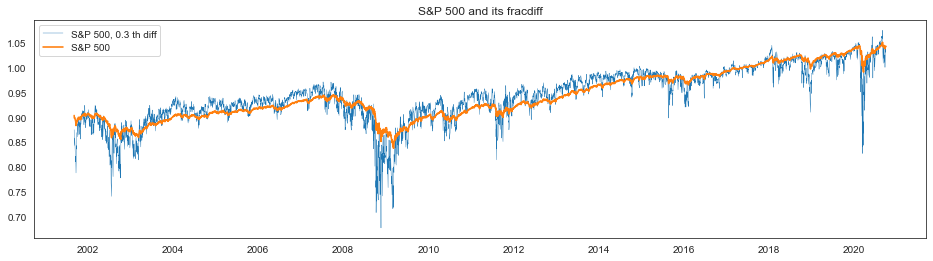

plt.plot(yd, linewidth=0.4, label=f"S&P 500, {d} th diff")

plt.plot(ys, linewidth=1.6, label="S&P 500")

plt.legend()

plt.title("S&P 500 and its fracdiff")

plt.show()

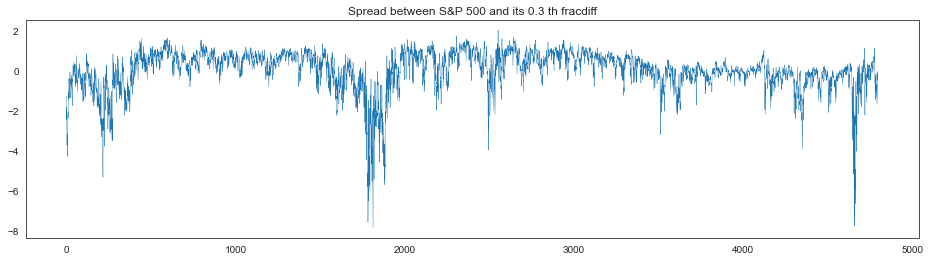

[39]:

spread = ca.transform(pair)

[40]:

plt.figure(figsize=(16, 4))

plt.plot(spread, linewidth=0.4)

plt.title(f"Spread between S&P 500 and its {d} th fracdiff")

plt.show()

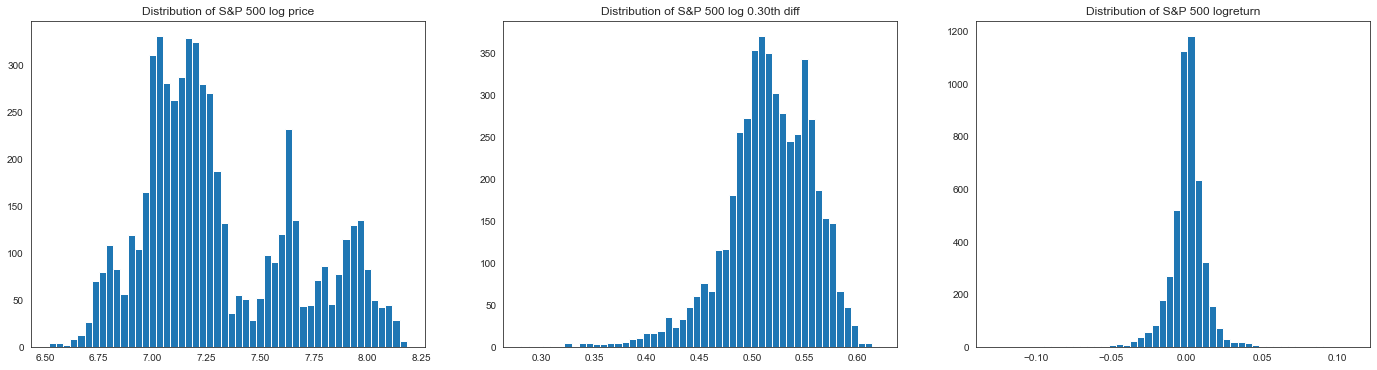

5.5 (e)#

[41]:

from statsmodels.stats.stattools import jarque_bera

[42]:

spxlogd.values.reshape(-1, 1).shape

[42]:

(4798, 1)

[43]:

X = spxlog.values.reshape(-1, 1)

f = FracdiffStat(window=window, mode="valid")

spxlogd = pd.Series(f.fit_transform(X).reshape(-1), index=spx.index[-diff.size :])

spxlr = spxlog.diff()[-spxlogd.size :] # logreturn

pd.DataFrame(

{

"S&P 500": jarque_bera(spx[-spxlogd.size :]),

"S&P 500 fracdiff": jarque_bera(spxlogd),

"S&P 500 logreturn": jarque_bera(spxlr),

},

index=["JB statistics", "p-value", "skew", "kurtosis"],

).round(3)

[43]:

| S&P 500 | S&P 500 fracdiff | S&P 500 对数收益 | |

|---|---|---|---|

| JB 统计量 | 637.418 | 1110.285 | 29941.995 |

| p 值 | 0.000 | 0.000 | 0.000 |

| 偏度 | 0.873 | -0.834 | -0.445 |

| 峰度 | 2.629 | 4.664 | 15.206 |

[44]:

plt.figure(figsize=(24, 6))

plt.subplot(1, 3, 1)

plt.title("Distribution of S&P 500 log price")

plt.hist(spxlog, bins=50)

plt.subplot(1, 3, 2)

plt.title(f"Distribution of S&P 500 log {d:.2f}th diff")

plt.hist(spxlogd, bins=50)

plt.subplot(1, 3, 3)

plt.title("Distribution of S&P 500 logreturn")

plt.hist(spxlr, bins=50)

plt.show()

[ ]: